Level 3 payment processing is a term used in credit card processing that refers to a deeper level of transaction data being transmitted to the payment processor. This type of processing is designed to provide additional information to the processor to help reduce processing costs and minimize the risk of fraud and chargebacks. In this article, we cover what Level 3 processing is, how it works, why it’s important, and who uses level 3 payment processing.

What is level 3 payment processing?

Level 3 payment processing is a type of credit card processing that is designed for high-value B2B (business-to-business) transactions. It is named “Level 3” because it involves a higher level of data and information than traditional credit card processing.

When a business accepts a Level 3 credit card transaction, it captures and transmits more detailed information about the transaction than a traditional credit card transaction. This information includes data such as item descriptions, quantities, and purchase order numbers, which are necessary for businesses to conduct B2B transactions.

This additional information is used to provide more detailed transaction data to the card issuer and merchant acquirer, which can help reduce the risk of fraud and chargebacks. It also provides useful data for businesses to track and manage their expenses.

Level 3 processing requires a specialized payment gateway that can capture and transmit the additional transaction data. It also typically involves lower processing fees than traditional credit card processing, due to the lower risk of fraud and chargebacks associated with B2B transactions.

What extra data is included in a level 3 transaction?

Level 3 payment processing captures and passes more detailed data about a transaction than traditional credit card processing. This additional data includes:

Item descriptions: This involves a detailed description of the items being purchased, such as the product name, model number, and unit price.

Quantities: This includes the quantity of the items being purchased.

Purchase order number: This is a unique identifier for the purchase, which is typically used by businesses to track and manage their expenses.

Tax information: This includes the tax amount and tax rate for the transaction.

Shipping information: This includes the shipping address and shipping method.

Merchant information: This involves the merchant’s name, address, and tax identification number.

By capturing and passing this additional data, Level 3 payment processing provides more detailed information about a transaction which can be very useful for businesses.

How does level 3 credit card processing work?

When a business accepts a Level 3 credit card transaction, the additional information is captured and transmitted along with the standard credit card information, such as the card number, expiration date, and security code. This information is then sent to the merchant’s payment processor, which verifies the transaction and sends it to the card issuer for approval.

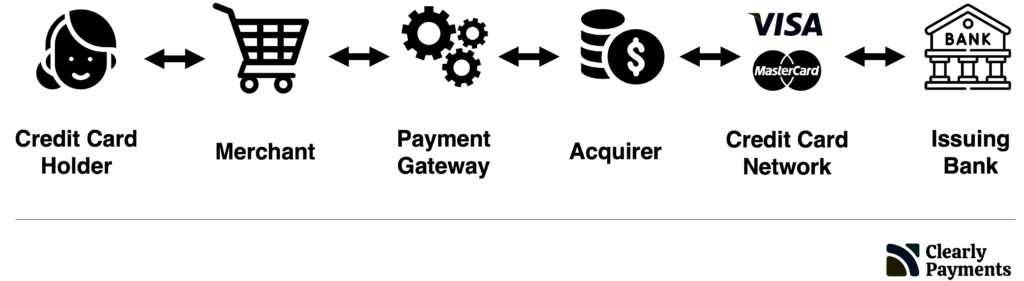

- Credit Card Holder: The person who owns the credit card submits a transaction through a merchant’s POS, eCommerce site, software, or other transaction tools.

- Merchant: The business has a point of sale that the credit card holder interacts with.

- Payment Gateway or Credit Card Machine: The payment gateway or credit card machine is the software or hardware that facilitates the payment from the business. The payment gateway or credit card machine is provided by a merchant services provider like TRC-Parus. This step validates the consumer’s credit card and routes the level 3 transaction information to the Acquirer.

- Acquirer: The acquirer is the “bank” that underwrites the merchant, meaning it takes on the risk in providing credit to the merchant. The acquirer processes the credit card payment and routes it to the actual credit card network such as Visa, Mastercard, Discover, or American Express.

- Credit Card Network: The credit card network does verification on the validity of the credit card and communicates with the issuing bank, which is the bank that provided the credit card to the consumer.

- Issuing Bank: The issuing bank provides the credit to consumers. The issuing bank will validate that the credit card is in good working order and validates there is enough balance of funds on the credit card to approve the transaction.

Why is level 3 payment processing important?

Level 3 processing is designed to help businesses reduce the costs associated with credit card processing. By including additional data in the transaction, the processor can determine the most cost-effective interchange rate, which can result in lower processing fees. Additionally, by providing more detailed information, Level 3 processing can help reduce the risk of fraud and chargebacks, which can also result in lower costs for merchants. Here are the key values that level 3 processing provides:

Improved transaction security: Level 3 processing captures more detailed transaction data, which helps to reduce the risk of fraud and chargebacks. This is particularly important for high-value transactions, which are more attractive to fraudsters.

Lower processing fees: Because Level 3 processing provides more detailed transaction data, it is considered to be a lower risk for card issuers and merchant acquirers. This means that Level 3 processing typically has lower processing fees than traditional credit card processing.

Better data for tracking and managing expenses: Level 3 processing captures more detailed transaction data, including item descriptions, quantities, and purchase order numbers. This information is useful for businesses to track and manage their expenses, particularly for B2B transactions.

Compliance with regulations: Some industries, such as government contracting, require Level 3 processing for certain types of transactions in order to comply with regulations.

What type of business uses level 3 processing?

Level 3 processing is used by businesses that process high volumes of B2B (business-to-business) transactions or by government entities. Here are some examples of businesses that commonly use level 3 payment processing:

Government agencies: Federal, state, and local government agencies often use level 3 processing for procurement and other transactions.

B2B merchants: Businesses that sell goods or services to other businesses often use level 3 processing, particularly if they have large or recurring transactions.

Wholesale distributors: Distributors that supply products to other businesses often use level 3 processing, as it can help reduce the cost of accepting credit card payments.

Manufacturers: Companies that produce goods for other businesses often use level 3 processing to streamline the purchasing process and reduce costs.

Corporate purchasing departments: Large corporations often use level 3 processing for their procurement departments to manage and track purchasing expenses.

Keep in mind that not all payment processors offer level 3 processing, so you’ll need to check with your payment processor or merchant services provider to see if it’s available. Additionally, you’ll need to meet certain requirements to qualify for level 3 processing, such as providing detailed transaction data and using specific types of credit card terminals or software.

How to get level 3 payment processing?

The TRC-Parus merchant account supports level 3 payment processing. We can offer the simplest, most efficient, and low cost level 3 credit card processing. Click here to sign up for a merchant account now.