In today’s digital age, electronic payment methods have become increasingly prevalent in our daily lives. Whether it’s swiping a credit card, making an online purchase, or tapping a smartphone at a checkout terminal, these transactions involve a complex network of processes working behind the scenes.

One crucial element that facilitates smooth and secure payment processing is the Merchant ID (MID). In this article, we will explore what a Merchant ID is, how it works, and its significance in the world of credit card payments.

What is a Merchant ID?

A Merchant ID, commonly abbreviated as MID, is a 15 digit unique identification number assigned to a business or merchant by a payment processor. A merchant ID is the number for a merchant account.

A merchant ID serves as an essential link between the merchant and the payment system, enabling seamless and secure electronic transactions. Think of the MID as a digital fingerprint that distinguishes each merchant from others within the payment processing ecosystem.

Where to find your merchant ID

Finding your merchant ID typically depends on the payment processor that you are using. Here are some common ways to find your merchant ID:

Merchant Dashboard or Portal: Most payment processors provide a merchant dashboard or portal where you can access and manage your account information. Log in to your account on the payment processor’s website and navigate to the account settings or profile section. Your merchant ID should be displayed there.

Merchant Agreement: Your merchant ID is often included in the merchant agreement or contract you signed when you set up your payment processing services. Check your records for any documents provided by the payment processor during the onboarding process.

Statements or Invoices: When you receive regular statements or invoices from your payment processor, your merchant ID is listed on these documents. Look for any reference to your merchant account number or identification.

Physical Terminal or Device: If you have a physical card terminal or payment device, the merchant ID is likely displayed on the device itself or accessible through its settings menu.

Credit Card Receipts: Another common place to find your merchant ID is on the top section of your credit card receipts that you give to customers, just after the “Terminal” information.

Remember that the location and method of accessing your merchant ID may vary depending on the payment processor you are using, so refer to the specific procedures and resources provided by your payment service provider. Additionally, ensure that you protect this information as it is sensitive and essential for secure payment processing.

How does a merchant ID work?

The MID plays a crucial role in facilitating payment processing and is used to associate and track transactions made by a specific merchant. Here’s how a merchant ID works in the payment processing ecosystem:

Application and Account Setup: When a business applies for payment processing services, the payment processor or acquiring bank assigns a unique MID to the merchant upon approval of their application. This MID serves as an essential link between the merchant and the payment processor.

Transaction Initiation: When a customer makes a purchase using a credit card, debit card, or other electronic payment methods at the merchant’s point of sale (POS) or online store, the payment process begins. The payment terminal or payment gateway sends the transaction details, including the MID, along with other necessary information to the payment processor.

Routing and Authorization: The payment processor receives the transaction request and processes it based on the merchant’s MID. It routes the transaction to the appropriate card network (e.g., Visa, Mastercard) for authorization. The card network verifies the card details, checks for available funds, and confirms whether the transaction can proceed.

Transaction Settlement: After obtaining authorization from the card network, the payment processor proceeds to settle the transaction. This involves transferring the funds from the customer’s account to the merchant’s account. The MID is again used to ensure that the funds are credited to the correct merchant account.

Reporting and Reconciliation: The MID is vital for tracking and reporting transactions made by the merchant. It allows the payment processor to generate detailed reports and statements for the merchant, providing insights into sales volume, revenue, and other essential transaction data. Merchants can use this information for accounting, financial analysis, and business planning.

Chargebacks and Disputes: In the event of a chargeback or payment dispute, the MID helps the payment processor to identify the specific merchant involved in the transaction. This assists in the resolution process and ensures that any chargebacks are appropriately allocated to the respective merchant account.

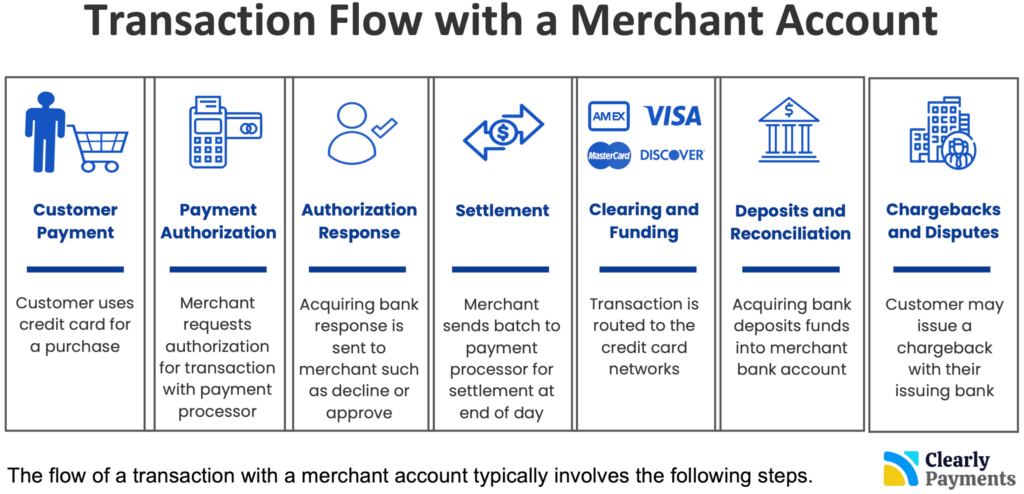

This is a high-level overview of how a transaction works with a merchant ID or merchant account. There are many players involved in a transaction, including many 3rd party software and hardware components. Here’s an overview of the payment processing industry and value chain.

Significance of Merchant IDs

- Uniqueness and Accountability: Each merchant is assigned a unique MID, which ensures that their transactions are traceable and accountable. This traceability is vital for financial record-keeping, auditing, and resolving potential disputes.

- Fraud Prevention: Merchant IDs play a crucial role in fraud prevention. By associating specific transactions with a particular merchant, payment processors can detect suspicious patterns and activities more effectively, protecting both the merchant and the cardholder.

- Payment Routing: Merchant IDs are used to route transactions to the correct merchant’s account. This accuracy is essential, especially in cases where multiple merchants use the same payment processor or acquiring bank.

- Reconciliation: Merchants rely on their Merchant IDs to reconcile their daily or periodic transaction reports with the payments they receive. This process helps them ensure that all transactions have been correctly processed and accounted for.

- Account Management: Payment processors and acquiring banks use Merchant IDs to manage and maintain merchant accounts efficiently. This includes handling chargebacks, refunds, and other account-related activities.

Can businesses have multiple merchant IDs?

Businesses can have multiple merchant IDs. One common reason for having multiple merchant IDs is when a business operates multiple business units or maintains several physical locations. In such cases, obtaining separate merchant IDs for each unit or location allows the business to better track and report transactions for each entity independently, facilitating more effective financial management.

Furthermore, businesses that operate through diverse sales channels, such as e-commerce platforms, brick-and-mortar stores, and mobile sales, often have different merchant IDs for each channel. By doing so, they can gain insights into the performance of individual sales channels and track revenue streams separately, enabling more targeted decision-making and resource allocation.

Another scenario in which multiple merchant IDs are used is for businesses involved in international transactions dealing with different currencies. Having separate merchant IDs for various currencies simplifies accounting and mitigates potential complexities arising from currency conversions, ensuring smooth and transparent financial operations.

What is the difference between a MID and a TID?

In the realm of payment processing and merchant accounts, two significant identifiers are often used: the Merchant Identification Number (MID) and the Terminal Identification Number (TID).

The MID serves as a unique identifier assigned to a merchant or business by the payment processor or acquiring bank, enabling them to distinguish one merchant from another within the payment processing system. It remains constant and is associated with the merchant’s account, representing their ongoing relationship with the payment processor.

On the other hand, the TID is a distinct identifier assigned to individual payment terminals or point-of-sale (POS) devices used by the merchant. Each terminal is given its own TID, allowing for differentiation within the same merchant account. Unlike the MID, the TID can change if the merchant acquires a new terminal or updates existing ones.