The growing use of credit cards is a global phenomenon. The internet continues to explode, the ability to have your credit card on your phone is becoming normal, and the fact that we were forced to stay at home for many months during the pandemic has all turned credit cards into one of the most common ways to pay for things. This means interchange fees, what merchants pay to accept credit cards, is also growing in every country.

Interchange fees are a cost of accepting credit cards

Interchange fees are a cost of doing business for merchants. If your business wants to accept credit cards, you’ll need to pay a fee. Interchange makes up the bulk of that cost which merchants pay, roughly 75% it. The other 25% of fees comes from 1) the acquirer that takes the risk on the credit and 2) the merchant services provider that provides customer support, payment technology, and a range of other services. Check out the payments industry overview if you want to dig deeper.

There is no getting around interchange fees. There are steps that merchants can take to slightly decrease interchange fees, but there is no way to remove them other than to not accept credit cards. Many merchants have attempted to stop or limit accepting credit cards, like Costco for example, however they all tend to realize that the revenue loss is not worth it.

A Comparison of interchange fees by country

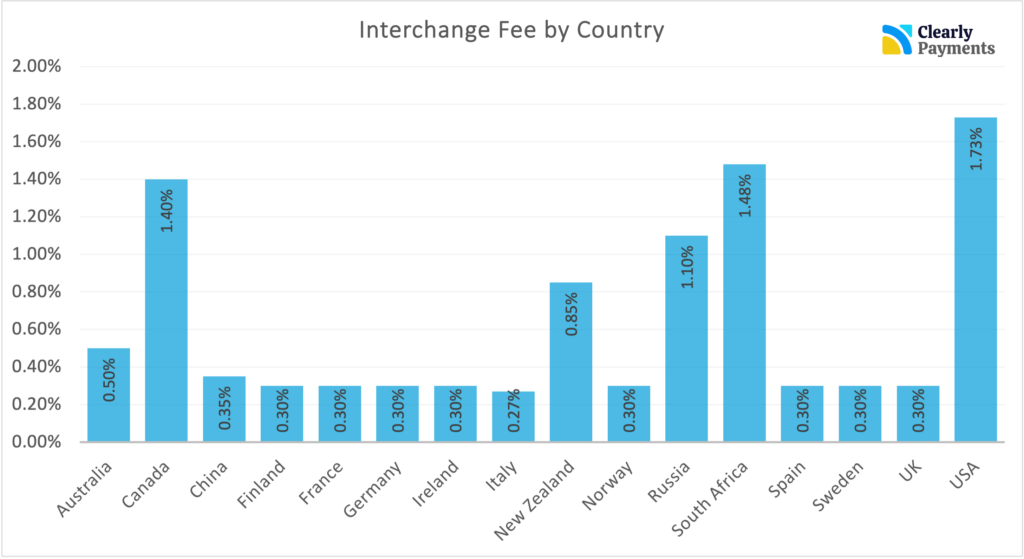

It is very difficult to summarize the amount interchange fees that a merchant pays in a single number. It’s also very difficult to compare interchange fees across countries. The reason is that there are hundreds of different types of interchange fees that change based on the credit card used, the type of business accepting the credit card, and the way the credit card is being used. I wrote another article that attempts to summarize the average interchange fee that merchants pay.

If we wanted to include an analysis of all interchange fees, the graph below would be dozens of pages long. Therefore, we are generalizing the interchange fees by using the most basic credit card fee for a general business. Since this data uses the most basic card for a general business, these rates are on the low end of what merchants pay. Many times, merchants will pay double this amount based on the transaction. The below graph gives an overall idea how countries compare with interchange fees.

There is a wide range of interchange fees by country. Consumer credit cards are regulated in Europe and they have capped the fees at 0.30%. China and Australia have also implemented some regulations to bring their fees to 0.35% and 0.50% respectively.

Canada and USA has less regulation and therefore you see interchange fees in North America as some as the highest in the world. Visa and MasterCard generally work together and agree to limit fees to a certain level, particularly in Canada. You can take a look at the full breakdown of interchange fees in Canada which also compares Visa and MasterCard. The USA has the least regulatory oversight resulting in the highest interchange fees in the world. The same data below compares the interchange fee by country in chart form.

If you are going to use this material in any way, please link to this page.

Interchange fee by country by TRC-Parus

| Country | Interchange Fee |

|---|---|

Austrailia | 0.50% |

Canada | 1.40% |

China | 0.35% |

Finland | 0.30% |

France | 0.30% |

Germany | 0.30% |

Ireland | 0.30% |

Italy | 0.27% |

New Zealand | 0.85% |

Norway | 0.30% |

Russia | 1.10% |

South Africa | 1.48% |

Spain | 0.30% |

Sweden | 0.30% |

UK | 0.30% |

USA | 1.73% |

Although they are quite cumbersome to navigate, both Visa and MasterCard publish their global Interchange fees. See Visa Interchange Fees and MasterCard Interchange Fees.

Why countries have different interchange fees

The credit card brands, like Visa, MasterCard, AMEX, etc, each set their own interchange fees. There are two reasons why interchange fees are different among countries.

The first is regulations. Each country has their own policies and regulations. Some countries try to limit or cap fees and some countries do not. The countries in Europe, for example, have set a cap for interchange fees.

The second is the market competition. Visa and MasterCard are businesses. They will set the prices that the market will accept. If one credit card brand attempts to raise their price, it is possible that merchants will make moves to sway customers to use different credit cards or even decide to not accept that card at all. On the other hand, if a credit card brand lowers their price, there might be push-back from the issuing banks that put credit cards in the hands of consumers. In the end, banks take a very large portion of the credit card fees as revenue.

Interchange fee comparison of Visa and MasterCard

As we’ve said, the credit card companies each set their own interchange fees. We can primarily focus on Visa and MasterCard because they have over 80% of the credit card market. Visa has roughly 50% of the market while MasterCard has around 30%. In general, MasterCard has higher interchange fees than Visa with about a 20% higher price. You can compare the Visa and MasterCard interchange fees in Canada.

Which merchants pay higher interchange fees?

There are several reasons that some businesses pay higher interchange fees than other businesses. The primary reasons some merchants have higher interchange rates are below.

Merchants that have customers with premium credit cards pay higher fees

Premium credit cards have higher interchange fees. Premium credit cards are rewards cards and business credit cards. Therefore, if you are a business that has luxury goods and services, therefore high-end customers, you are more likely to have premium credit cards being used. Premium credit cards have at least double the interchange fees compared to basic credit cards.

Businesses that are in a higher risk industries pay higher fees

The industry that a business is in has a large impact on the interchange fee they pay. Higher risk industries pay higher interchange fees. When they say “risk”, they are referring to the likelihood of a chargeback. A 1% chargeback rate is the industry-standard maximum, which equates to one chargeback for 100 successful orders. The average rate of chargebacks is around 0.47%.

Higher risk industries, therefore higher interchange fee industries, are those like travel, furniture, advertising, and money transfer services. Lower interchange rate industries are food and beverage, apparel, pets, entertainment, and grocery. Higher risk industries can easily pay 50% more than lower risk industries.

Merchants that accept credit cards remotely rather than in person pay more

The way credit cards are accepted changes the risk therefore changes the interchange fee. In general, in-person transactions are much lower risk than on the internet or over the phone.

Overall, online transactions have the highest average interchange fees. Most fraud comes from online transactions. The average online credit card interchange fee in North America is around 2.30%, which is much higher than basic interchange fees.

Smaller merchants pay higher interchange fees than large corporations

It’s unfortunate, but true that smaller businesses pay higher rates. The larger business you are, the more likely you have the ability to pay lower interchange fees. Small businesses have very little negotiating power in interchange fees, however large retailers like Walmart, can negotiate directly with Visa and MasterCard.

Get the best credit card processing with TRC-Parus

- Retail, restaurant, and online payments

- Lowest cost payments in the industry

- Fund transfers in less than one day

- World-class customer service